Key Takeaway

End-to-End Loan Approval Orchestration

Discover how to seamlessly combine eligibility checks, credit scoring, and dynamic pricing into a single automated workflow using the DecisionRules.io API-driven BRMS.

Total Risk Control

Empower Risk Managers to adjust the flow, add A/B tests, or modify logic without waiting for IT.

Ready-to-Use Framework

Leverage pre-built templates for every stage of the loan lifecycle to launch faster and reduce errors.

Total Control of Lending in One Flow

In our previous articles, we broke down the individual components of the credit process—from scoring to pricing. Now, we bring them together.

By combining these templates into a single workflow, Risk Managers can finally achieve the “Holy Grail of Lending", a complete Loan Approval process that is fully under your control, transparent, and flexible enough to adapt to market changes in minutes, not months.

Why specialized tools aren't the ultimate cure

In traditional lending systems, credit decisioning logic was often hard-coded. Any change to the Loan Approval process required technical intervention, resulting in a slow and rigid change management process.

When specialized Credit Decisioning tools (both traditional giants like Experian or FICO and newcomers like Pega or Actico) entered the market, they promised agility. They put some setup capabilities into the hands of risk analysts, shortening the change process. However, these tools often come with a hidden cost: rigidity.

- Heavy-weighted architecture: They are often complex and expensive to maintain.

- Fixed Patterns: Components like scorecards or rule sets are often pre-defined. They give you a "flavor" of freedom, but not the full taste.

With universal Business Rule Engines like DecisionRules, true freedom of design is finally possible. But does this mean you have to build everything from scratch? Not at all.

Building Your Complete Loan Approval Process from DecisionRules Templates

With DecisionRules, you don't start from scratch. Our flexible, no-code templates provide a guided framework, allowing Risk Analysts to design a complete loan approval process tailored precisely to your institution's needs. This unified approach eliminates silos and accelerates change.

Process steps:

- 2. Eligibility Rules: Evaluate rules deciding whether the client is eligible for a loan or not using Eligibility and Policy Rules template.

- 3. Scoring: Assess the client’s probability of default by calculation of the client score using: Dynamic Score Calculation and Client Scorecard templates.

- 4. Loan Parameters & Pricing: Determine the client's capacity to borrow by assessing the client’s financial situation against limits. Set the final Interest Rate based on client score and loan parameters. Calculate installment amount and APR. These calculations are performed by orchestrating the following templates: Affordability and Limits Calculation, Risk Based Pricing and Loan Calculator

- 5. Policy Rules: Evaluate rules deciding whether the application is to be declined, approved automatically, or handed over to manual underwriting using Eligibility and Policy Rules template.

By linking these powerful, customizable templates sequentially within a single Decision Flow, your risk team gains full end-to-end control, easily adapting the lending process to specific needs and market dynamics.

Orchestrating Your Lending Process

Building your Loan Approval process in DecisionRules involves assembling individual modules and orchestrating their execution within a central Decision Flow. This allows you to define a logical sequence for every step, ensuring consistency and control.

A typical Loan Approval design often encompasses these critical steps:

- A/B Testing Setup: Implement testing groups to evaluate the performance of different rule sets or strategies.

- Eligibility Rules Evaluation: Apply criteria to determine an applicant's basic loan eligibility.

- Score Calculation: Compute a client's risk score based on various data points.

- Affordability and Loan Parameters Calculation: Determine loan amounts, terms, and pricing based on the client's financial capacity.

- Policy Rules Evaluation: Enforce business policies to arrive at the final loan decision.

Let's explore the A/B Testing Setup in more detail within this orchestrated flow.

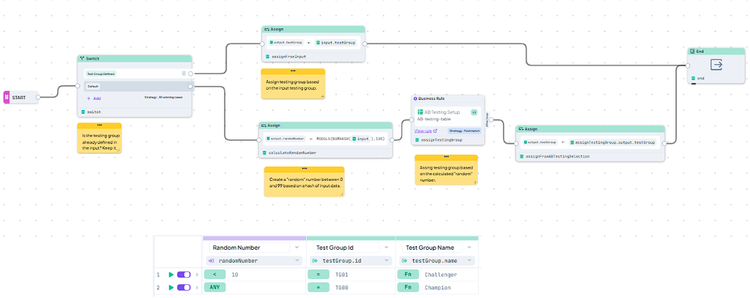

A/B Testing Setup in Action

The "AB Testing" template is a key component for dynamic process management. As seen in our guide A/B Testing in Credit Risk, it lets you define testing groups that can influence the execution path of your Decision Flow. For instance, you can:

- Assign Test Groups: Based on an incoming application's data, or through internal logic, categorize applicants into different test groups (e.g., "Champion" vs. "Challenger").

- Dynamic Rule Execution: Route applicants from specific test groups through different sets of eligibility, scoring, or pricing rules to evaluate their effectiveness.

- Continuous Optimization: By observing the outcomes, you can continuously refine your lending strategies.

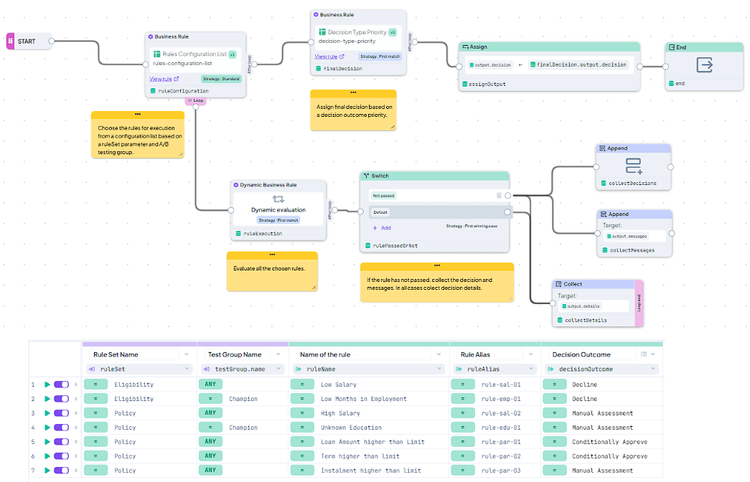

This setup is fully integrated into the Decision Flow, as illustrated in the overview below, providing a flexible way to manage different scenarios and optimize performance.

Fig.1: A/B testing template overview - setup of test groups in Decision Table and orchestration of test groups assignment in Decision Flow

Eligibility and Policy Rules

In our guide on Eligibility and Policy Rules, we demonstrated a template for creating robust rules, grouping them into logical sets, and executing specific rule sets on demand.

This template is reused twice in our sample Loan Approval process:

- First: To evaluate Eligibility rules (initial knock-out criteria).

- Second: To evaluate Policy rules (final decisioning).

The mechanism remains identical; the only change is the `ruleSet` variable you wish to execute. This reusability significantly simplifies maintenance.

Note: A/B testing is applied directly at the rule set definition level, allowing you to test different policy criteria against each other.

Fig.2: Eligibility and Policy Rules template overview - setup of rule sets in Decision Table and orchestration of rule evaluation in Decision Flow

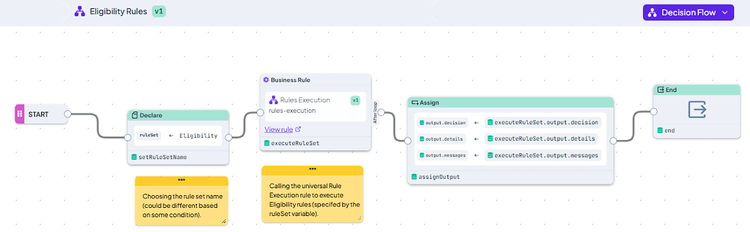

Fig.3: Use of the rule set execution template for evaluating Eligibility rules

Scoring

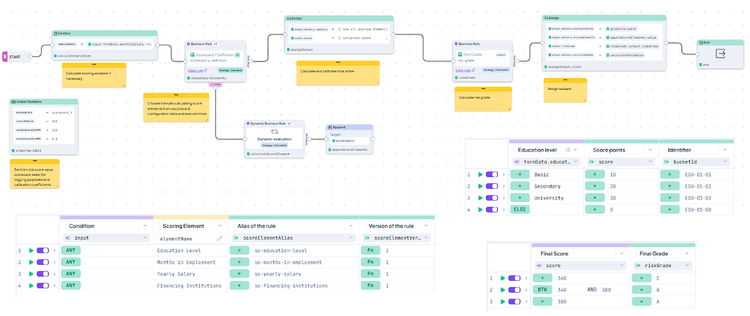

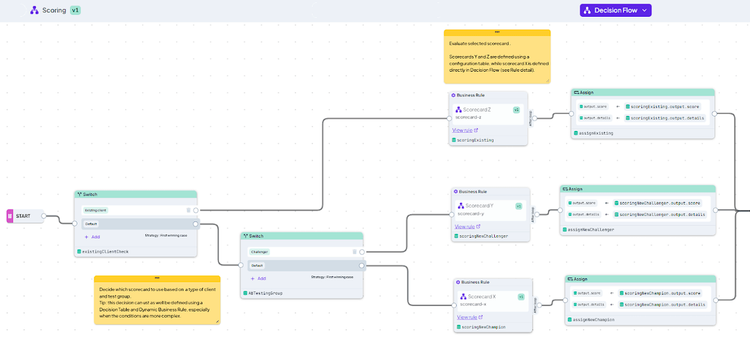

When configuring this risk assessment phase, we recommend building a no-code credit scorecard architecture that empowers risk analysts to manage weights and logic without IT dependency. As detailed in that guide, we offer two primary patterns for scorecard design. Our sample case utilizes both patterns and adds a layer of intelligence: a decision node that selects which scorecard to use based on specific applicant parameters or their assigned A/B Test Group.

Fig. 4: Overall picture of the Client Scorecard template

Fig. 5: Overall picture of the Dynamic Score Calculation template

Fig. 6: Selection of scorecard process that will be used

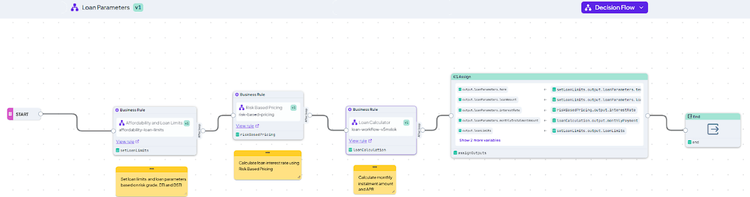

Affordability and Loan Parameters

As shown in our article on Affordability and Loan Parameters, there are several patterns to calculate a client's affordability and final loan terms. In our unified workflow, we connect these patterns into a single sequence that orchestrates them seamlessly.

Note: A/B testing is applied inside these patterns to test different limits (e.g., DTI caps) or interest rate strategies.

Fig. 7: Decision Flow joining Affordability and Limits Calculation, Risk Based Pricing and Loan Calculator into one process

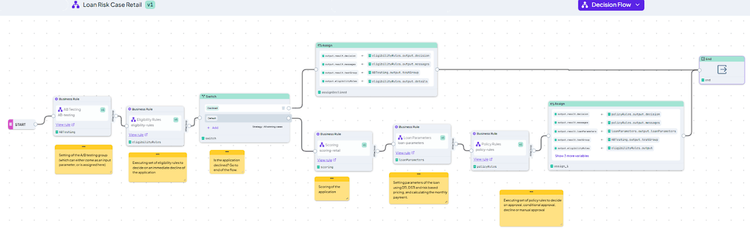

The Complete Loan Approval Process

The final step in designing your Loan Approval process is simply assembling the pieces. In our sample case, the steps described above are orchestrated in a single Decision Flow that executes them sequentially, passing the results of each step to the next.

Note: As mentioned above, the Eligibility and Policy Rules template is used twice within the flow: first to execute Eligibility rules, second to execute Policy rules.

Fig. 8: A sample Loan Approval process design

In this design, if any Eligibility rule is breached, the process stops immediately. However, thanks to the flexibility of DecisionRules, you could easily adjust the flow to complete all calculations anyway—perfect for monitoring purposes or "shadow running" new strategies. The design reflects *your* specific process, not a vendor's hard-coded logic.

Your Path To Modern Lending

DecisionRules built-in Loan Approval templates give financial institutions the power to design complete processes from predefined components. These can be easily adjusted to match your company’s exact needs, allowing you to govern and maintain all logic in one place. This ensures flexibility, transparency, and compliance for the whole process.

About the Author: Karel Svec is a Solution Consultant at DecisionRules with over 19 years of experience helping businesses manage their decisioning logic and improve efficiency. He specializes in solutions for credit decisioning, risk management and other financial use cases.

Karel Svec is a Solution Consultant at DecisionRules with 20 years of experience helping businesses manage their decisioning logic and improve efficiency. For 13 years, he acted as a Team Leader and Manager of Decision Sciences / Risk Infrastructure in the banking sector, being responsible for design of the credit decisioning infrastructure, implementation of lending rules and integration to credit bureau services. Utilizing this experience, he specializes in solutions for credit decisioning, risk management and other financial use cases.