Key Takeaway

Eliminate System Fragmentation

Replace siloed scoring, pricing, and calculation engines with a single, unified decision flow

3 Ready-to-Use Templates

Instantly deploy Affordability & Limits, Risk-Based Pricing, and Loan Calculator templates without starting from scratch.

Zero-Code Agility

Empower Risk and Product teams to adjust credit logic and pricing matrices without waiting for IT development.

The Missing Link in Credit Decisioning

You've approved the loan. But now comes the harder question: How much can this customer actually borrow? And at what rate?

Many risk managers view the calculation of loan parameters, balancing current exposure, income, regulatory limits (DTI/DSTI), and risk-based pricing , as a "black box" that is impossible to manage transparently.

DecisionRules changes this narrative. We provide three complementary, no-code templates that automate the entire calculation of credit parameters, turning a complex construction into a transparent workflow.

Why Fragmented Loan Calculation Kills Agility

Picture this: Your product team wants to test a new pricing tier for low-risk borrowers. Simple request, right? Except it requires changes in three different systems, coordination across two IT teams, and a six-week deployment cycle. By the time you launch, the market opportunity has passed.

In traditional lending architectures, calculating the parameters required for a final credit offer involves a relay race between multiple, siloed systems:

- The Scoring System: Decides on eligibility and calculates basic limits (e.g., maximum term, Debt-to-Income ratio) within the affordability calculation.

- The Pricing Engine: A separate system that determines the interest rate based on risk score inputs and specific loan parameters.

- The Calculation Tool: A third system performs the amortization math to finalize the monthly installment.

The Result? A fragmented, sequential process that is prone to error. A simple change to an affordability rule often triggers a cascade of broken logic downstream. This makes pricing adjustments slow, disorganized, and heavily dependent on IT intervention.

How to Unify Loan Decisioning in One Platform

The DecisionRules approach replaces this fragmented "relay race" with three integrated, no-code Decision Flow templates. These automate the entire lending parameter stack in a single, coherent workflow, ensuring that changes in one area automatically reflect in the others.

1. Template: Affordability and Limits Calculation

Purpose: Determines the client's capacity to borrow by assessing clients financial situation (income and expenses) against limits (Debt-to-Income, Debt-Service-To-Income).

Key Outputs:

- Maximum loan amount

- Maximum term and payment

- Loan amount and term

2. Template: Risk-Based Pricing (RBP)

Purpose: Sets the final Interest Rate based on client score and loan parameters

Key Outputs:

- Interest Rate

3. Template: Loan Calculator

Purpose: Computes the final required Monthly Payment for the approved loan amount and term at the determined price.

Key Outputs:

- Monthly installment

- Total payable amount

- APR

By linking these templates sequentially in a single Decision Flow , risk and product teams can manage the entire lending logic end-to-end without writing a single line of code.

How DecisionRules Templates Work: A Deep Dive

1. Affordability and Limits Calculation Template

Example: A customer applies with €3,000 monthly income and €800 in existing obligations. The template instantly processes these inputs against your DTI rules and caps the maximum eligible loan at €15,000 over 36 months—no spreadsheet gymnastics required.

The Affordability and Limits Calculation template assesses a client's capacity to repay by analyzing their risk grade, income, existing payments, and exposure. It then calculates precise loan limits in just a few steps:

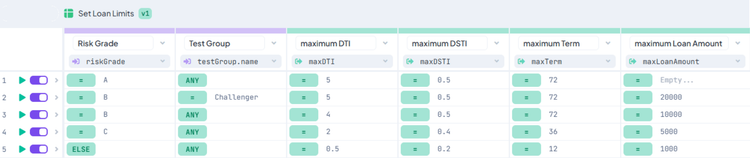

1. Dynamic Limit Determination: Utilizes a "Set Loan Limits" Decision Table to define maximum DTI, DSTI, loan term, and loan amount, dynamically adjusting based on the client's risk grade (and optionally, A/B testing groups).

Fig 1: Decision Table Set Loan Limit

2. Payment & Balance Aggregation: Consolidates all internal and external payments and outstanding balances.

3. Loan Limit Calculation: Determines the eligible loan amount based on Debt-to-Income (DTI) and Debt-Service-to-Income (DSTI) ratios, along with the maximum possible installment.

4. Parameter Comparison: Compares the calculated limits against the client's requested loan parameters to ensure compliance and feasibility.

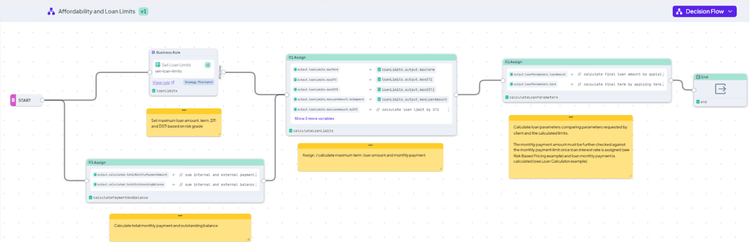

All these steps are seamlessly orchestrated within a dedicated 'Affordability and Loan Limits' Decision Flow, providing a transparent and auditable process.

Fig 2: Decision Flow Affordability and Loan Limits

2. Risk-Based Pricing (RBP) Template

Example: A "High Risk" applicant requests a €50,000 loan. The logic automatically detects their risk grade and applies a higher risk-based interest rate, increasing the APR from 9% to 14%. The system instantly recalculates the offer and returns a counter-proposal with the adjusted pricing—ensuring the bank maintains proper risk-adjusted returns while still providing a compliant offer.

The Risk-Based Pricing template moves beyond a "one-size-fits-all" rate. It determines the optimal interest rate by correlating the client's Risk Grade with specific loan parameters, allowing you to deploy distinct pricing matrices for different customer segments.

The solution consists of two powerful components:

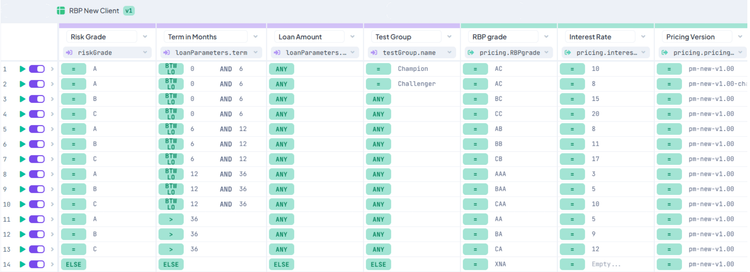

1. Configurable Pricing Matrices: Decision Tables like “RBP New Client” and “RBP Current Client” act as your pricing engine. They store your logic for assigning interest rates based on risk levels and loan characteristics.

Fig 3: Decision Table RBP New Client

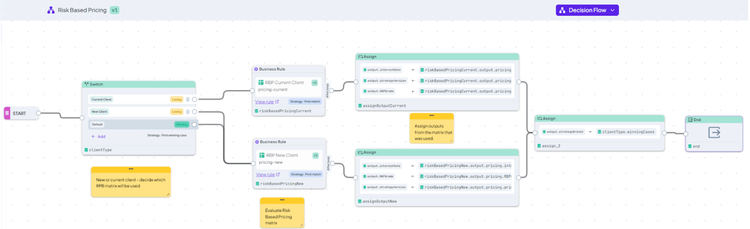

2. Intelligent Orchestration: The “Risk Based Pricing” Decision Flow acts as the brain. It evaluates customer attributes to select the correct pricing matrix, executes the lookup, and outputs the final interest rate automatically.

Fig 4: Decision Flow Risk Based Pricing

> Pro Tip: Because these are standard Decision Tables, you can update interest rates or add new pricing tiers in minutes, without needing IT deployment cycles.

3. Loan Calculator Template

Example: A client is approved for $10,000 over 24 months. The calculator not only computes the exact monthly installment of $452.27 but also factors in origination fees to generate the precise regulatory APR, ensuring your offer is fully compliant and ready for the contract in milliseconds

The Loan Calculator template goes beyond simply displaying a number; it manages the comprehensive calculation of loan installments, total payable amounts, and the Annual Percentage Rate (APR) based on the approved loan amount and term. This ensures transparency and compliance.

The calculation flow involves the following critical steps:

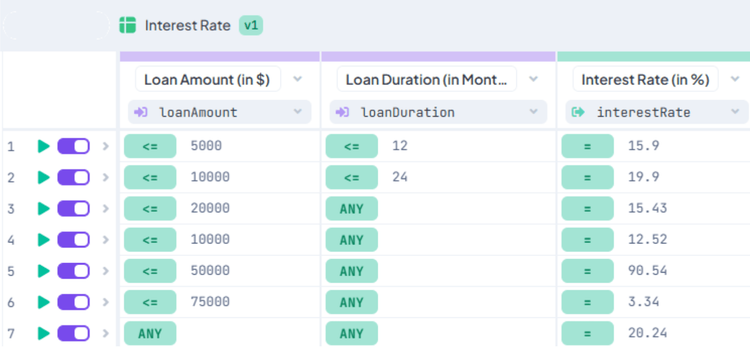

1. Interest Rate Determination: If not already provided by a Risk-Based Pricing model, the interest rate is dynamically calculated based on the loan amount and duration using a dedicated "Interest Rate" Decision Table.

Fig 5: Decision Table Interest Rate

2. Monthly Payment and Total Payment Calculation: A "Loan Calculator" Decision Table computes the exact monthly installment and the total amount payable over the loan's lifetime.

Fig 6: Calculation of the monthly payment

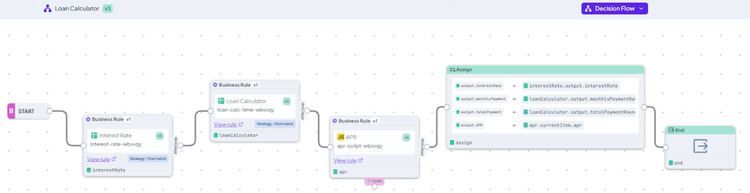

3. APR Calculation: A specialized Scripting Rule ("APR") accurately determines the Annual Percentage Rate, crucial for regulatory compliance and clear communication with the client.

Fig 7: Loan Calculator Decision Flow

This robust flow demonstrates how you can effortlessly handle complex financial calculations, such as annuity payments and APR, directly within DecisionRules. This eliminates the need for separate systems, ensuring all logic is centralized and auditable.

The Final Word: Unify Your Lending Logic

These three DecisionRules templates empower financial institutions to finally move beyond fragmented, cumbersome legacy systems. By seamlessly integrating Affordability, Risk-Based Pricing, and Loan Calculation into one dynamic, transparent process, you will:

- Gain Complete Control: Manage every aspect of your credit decisioning with unparalleled visibility.

- Reduce Time-to-Market: Rapidly launch new credit products and adjust parameters with business agility, not IT bottlenecks.

- Establish a Single Source of Truth: Ensure all loan parameter logic is centralized, consistent, and auditable across your organization.

About the Author: Karel Svec is a Solution Consultant at DecisionRules with over 19 years of experience helping businesses manage their decisioning logic and improve efficiency. He specializes in solutions for credit decisioning, risk management and other financial use cases.

Karel Švec

Business Analyst