Rigid credit scoring models and unwieldy Business Rule Engines frustrate risk analysts. This article reveals how DecisionRules’ no-code patterns empower business users to instantly update scoring criteria, transforming complex scorecards into flexible, well-governed systems. Discover how to achieve agility and reduce errors in credit risk management.

Why Credit Scoring Models Became an Unmanageable Mess

Scorecards are essential for decision-making in the loan approval process. As markets become more dynamic, the ability to adjust these scorecards instantly is critical.

Traditionally, any change to a credit scoring model, whether updating a variable or introducing a new risk grade, required slow and rigid technical interventions. This process was a significant bottleneck.

Business Rule Engines promised flexibility, but this freedom often leads to a new problem. Complex scoring logic, with dozens of variables and multiple scorecards, can quickly evolve into messy, unwieldy structures. This makes maintenance and auditing a nightmare, as it becomes difficult to track which variables are used where, or how changes to one scorecard might impact others.

Built-in Scoring Patterns That Actually Stay Organized

That disorderly, error-prone process is now obsolete. With the introduction of Client Scorecard and Dynamic Score Calculation patterns, you can now design and define your scorecard characteristics as well as the entire scorecard in a well organized, consistent manner.

You can find these templates in the Financial Services section of “Templates and Examples” modal in the DecisionRules app as well as in the Templates section of the web under the names Client Scorecard and Dynamic Score Calculation.

Fig. 1: Scorecard Templates in the Templates and Examples modal

Client Scorecard Template

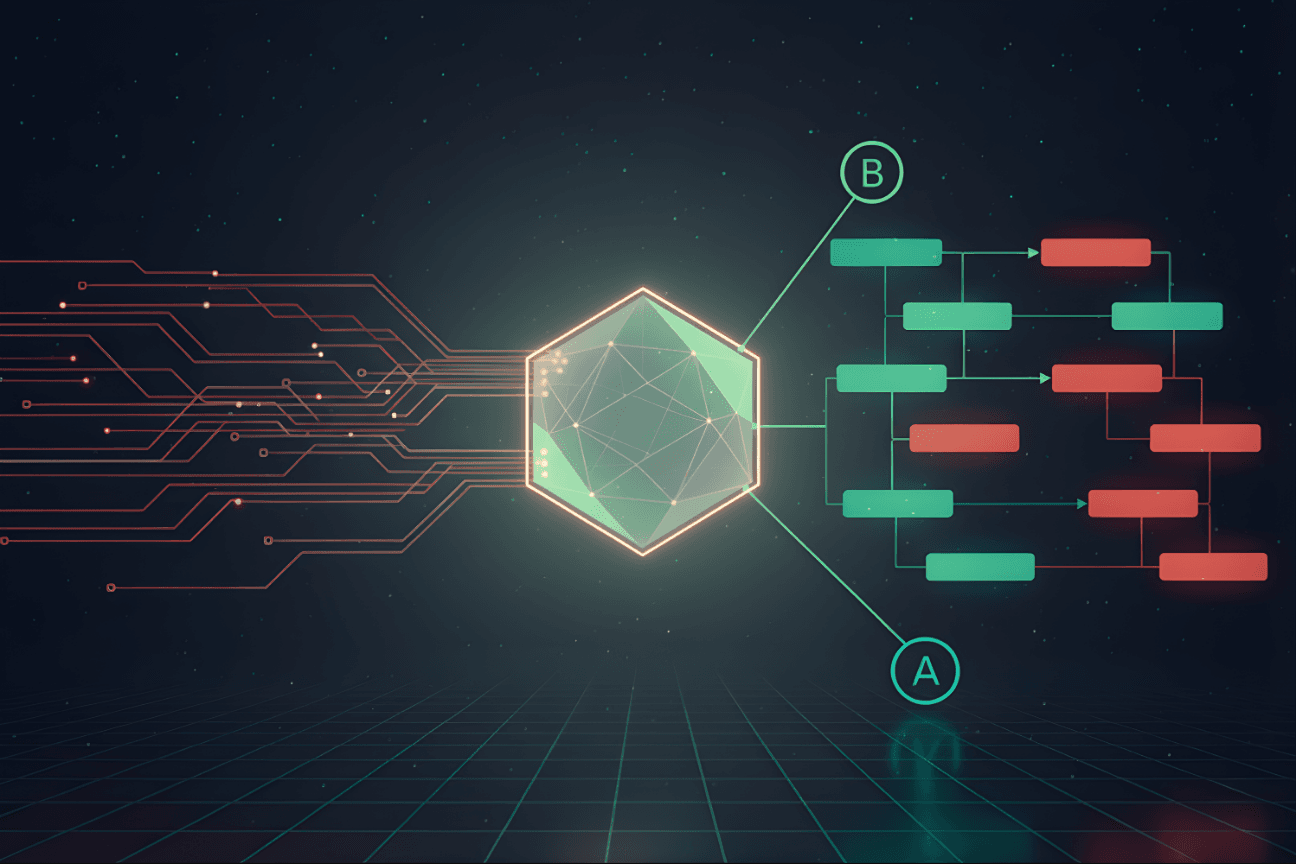

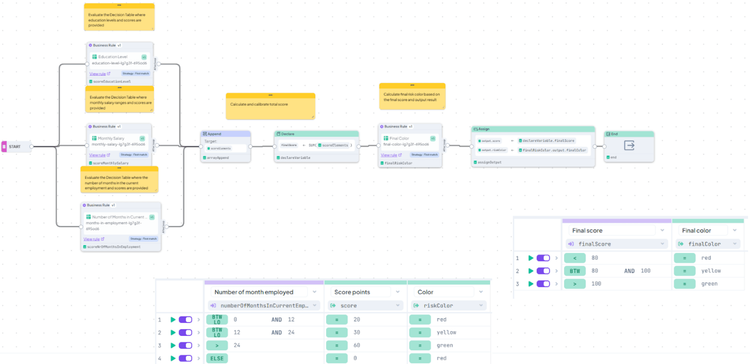

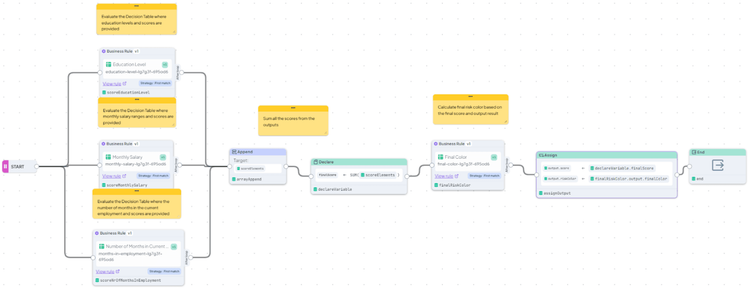

This template visualizes a scorecard in a Decision Flow, with each characteristic represented by a flow node. When the scorecard is run, you can directly view individual score points, the total score, and the risk color. Use this pattern for simpler scorecards where visualization is a priority.

Fig. 2: Overall picture of the Client Scorecard template

Dynamic Score Calculation Template

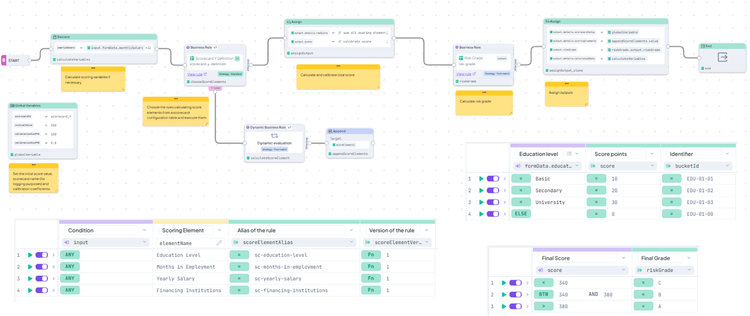

This advanced template offers a more dynamic and robust pattern for defining and executing scorecards. It produces bucket IDs for better auditability, defines scorecards in a Decision Table, and handles score calibration and risk grade assignment within the flow. Use this pattern to separate scorecard definition from execution logic, allowing you to add new characteristics by simply adding a new row to a table.

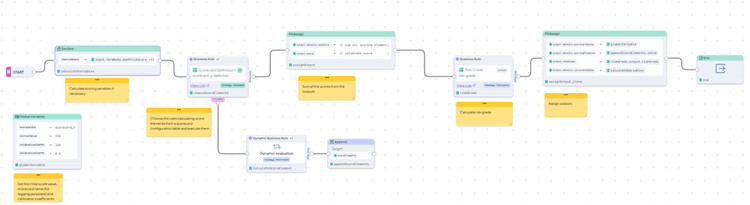

Fig. 3: Overall picture of the Dynamic Score Calculation template

| Feature | Client Scorecard (Easy Pattern) | Dynamic Score Calculation (Advanced Pattern) |

|---|---|---|

| Logic Design | Visual in the Decision Flow | Data-Driven in the Scorecard Definition Decision Table. |

| Flexibility/Scale | Lower. Requires updating the Decision Flow for every new scoring element. | High. Adding a new score element only requires adding a row to a Decision Table. |

| Advanced Features | No, only Risk Color is assigned. | Includes Variables Calculation, Score Calibration and explicit Risk Grade mapping. |

| Best Use Case | Simple, fixed-logic scorecards (e.g., initial risk assessment). | Complex, high-granularity, or rapidly changing credit models (e.g., large bank scorecards). |

Let's explore the detailed mechanics of these templates.

How to Structure Scoring Characteristics for Easy Updates

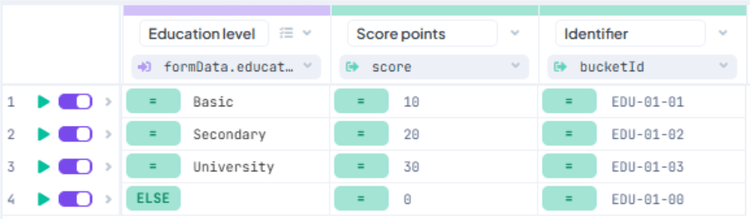

The foundation of every scorecard is a library of scoring characteristics. Both templates utilize separate Decision Tables for each characteristic, sharing a common structure that defines value ranges, assigned scores, and enriched outputs like bucket IDs or risk colors.

Fig. 4: Example of scoring table for Education level

This table efficiently checks the range into which a characteristic value falls, assigning the appropriate score and other outputs.

How to Define a New Scoring Characteristic (Dynamic Score Calculation Pattern)

To define a new scoring characteristic using the Dynamic Score Calculation pattern, follow these steps:

- In Folders, clone the Decision Table called “X - Template” in the “Score Elements” folder.

- In the Model tab of the table designer, adjust its Input Model to include the desired characteristic.

- In the Design tab, change the input attribute name in the conditions column to match the new characteristic, then adjust the score points and bucket ID.

- Add a new row for each scoring bucket, including characteristic values, score points, and bucket ID.

Two Ways to Build Credit Scorecards (and When to Use Each)

Next, let’s examine how scorecards are defined within each template.

Client Scorecard Template

Each scorecard is represented by a dedicated Decision Flow. This flow contains a Business Rule node for each scorecard characteristic, followed by nodes that aggregate the score and assign the final risk color.

Fig. 5: Decision Flow of Client Scorecard template

How to Add a New Scorecard Characteristic to the Client Scorecard

- On the canvas, create a new Business Rule node.

- Assign a Decision Table for the characteristic's score calculation and map the inputs.

- Connect the new node with the Start node and the Append node.

- Edit the Append node's settings to include the output of the newly defined Business Rule node in the “Values to append” section.

Dynamic Score Calculation Template

In this template, each scorecard is defined within a single Decision Table named "Scorecard Definition." This table lists all scorecard characteristics, specified by their aliases and versions of their respective Decision Tables.

Fig. 6: Scorecards definition in Dynamic Score Calculation template

The Decision Flow then orchestrates the execution of these Decision Tables as defined in the definition table, leveraging the functionality of a Dynamic Business Rule node. Additionally, the flow includes:

- A Global Variables node for defining initial scores and calibration coefficients.

- A Declare node for performing necessary calculations of scorecard characteristics.

- An Assign node for calculating the total score and performing calibration.

- A Business Rule node for assigning a Risk Grade, by calling a Risk Grade Decision Table.

Fig. 7: Decision Flow of Dynamic Score Calculation template

How to Add a New Scorecard Characteristic to the Dynamic Score Calculation Scorecard

- In the Scorecard Definition Decision Table, add a new row containing the scoring element name, alias, and version.

- (Optional) If the characteristic requires calculation, add a new row into the Declare node at the beginning of the Dynamic Score Calculation Decision Flow.

The Decision Flow will automatically read the updated list from the Scorecard Definition, execute your new rule, sum its score, and incorporate it into the final calibrated score and risk grade.

Note: When following this template's pattern, all input data and calculated data are automatically passed to the scorecard for execution, eliminating the need for manual mapping changes.

Upgrade your risk management experience

The Client Scorecard and Dynamic Score Calculation patterns are more than just a button; they are a direct upgrade to your risk management workflow that saves you time, reduces errors, and lets you focus on what actually matters—managing credit risk.

By leveraging the power of these templates to define your scorecard, you instantly achieve the flexibility and scalability required for modern financial services while ensuring consistency and keeping the change process under control.

About the Author: Karel Svec is a Solution Consultant at DecisionRules with over 19 years of experience helping businesses manage their decisioning logic and improve efficiency. He specializes in solutions for credit decisioning, risk management and other financial use cases.

Karel Švec

Business Analyst